Considering the U.S. industrial sector’s seemingly limitless success, industry outsiders might think industrial property owners, tenants and investors are just sitting back and reaping the rewards of a sophisticated global supply chain, impressive GDP and strong investment returns.

But not so fast. After attending the 2018 I.CON industrial conference a few weeks ago, I’ve been reflecting on why that assumption is grossly oversimplified, and what challenges we need to keep top of mind if we want the industrial sector to continue firing on all cylinders. We all know that planning ahead is what turns challenges into opportunities, so here are five areas that should be on everyone’s radar.

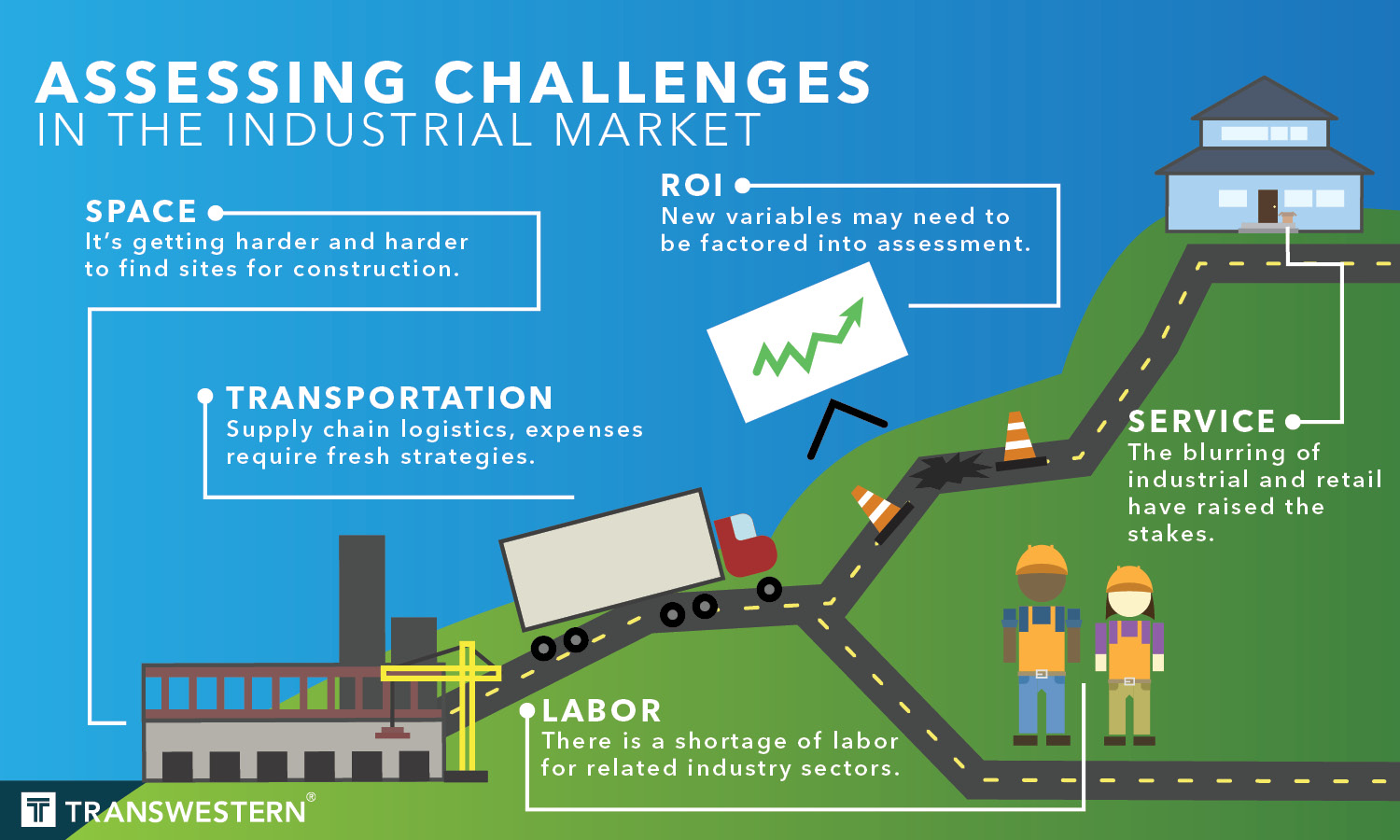

First, space (or lack thereof). Companies are insisting that warehouses be built within a one- or two-day drive of the customer – and with good reason. However, it’s getting harder and harder to find infill sites for construction, especially in big urban centers. If sites can be identified, they often come with greater capital needs driven by redevelopment and brownfield issues. Simply put, site selection is much different than it was a decade or two ago, and creativity is often the name of the game. Multi-story warehousing is only the beginning.

Second, transportation. This is a biggie, as transportation cost is a huge portion of the total supply chain expense – much larger, in fact, than real estate. Since the government stepped in to limit the number of hours for truck drivers, investment in autonomous vehicles has increased, but the fruition of the concept is still in the early stages. Expect a lot of discussion on this front going forward – and a huge transformation in how goods are moved from place to place. Because sending bigger trucks into tight urban centers isn’t going to do the trick.

Third, labor. Ensuring adequate labor is a real challenge, and we all know lack of labor can kill a deal. In this regard, we must be honest with landlords and tenants. The fact is, when the minimum wage goes up, it reduces the amount of talent available and increases the cost of real estate. The growing labor shortage does not only affect trucking. Workers need to be educated on employment opportunities in warehousing industries, because there are many. And it’s important to keep in mind that younger generations value a sense of purpose – companies must market to that.

Fourth, ROI. While we’ve wondered for years how high industrial rents could go, market rent growth in core coastal markets is expected to continue its upward trajectory. However, markets in the center of the country may be at or near the top, making for a riskier investment environment. This shouldn’t induce panic: We’re not at the end of the cycle, but certainly closer to the end than the beginning.

Last, but not least, service. In any industry, service is king. Customers have more option than ever before; therefore, it behooves every player in the industrial space to ensure they’ve incorporated service excellence into their culture. This begins in the very early stages, when lobbying for resident acceptance of a new warehouse development in a community all the way through to making sure deliveries arrive on the doorstop as promised. Communication and transparency is critical to building a strong brand – and increasingly so as the line between retail and industrial blurs.

Matthew Dolly, Director of Research

Parsippany, New Jersey